Revolut at Non-GamStop Casinos: When Deposits Go Through and When They Don’t

If you’d told me three years ago that Revolut would become one of the most discussed payment methods in the offshore casino space, I’d have asked you to repeat the sentence. Yet here we are. Revolut shows up in the cashier dropdown of a meaningful share of non-GamStop casinos, the question of whether a Revolut card will go through is one of the most asked questions in player forums, and the answer is genuinely complicated. It depends on what kind of Revolut card you’re using, what setting your account is in, which casino is taking the payment, and which payment processor sits in between.

Against a backdrop where the UKGC-regulated share of UK gambling has slipped from 97 per cent in 2019 to roughly 92 per cent by 2025, the payment-method question matters more than it used to. The audience using offshore is larger, and Revolut sits squarely in the middle of how that audience actually moves money.

How Revolut categorises gambling merchants

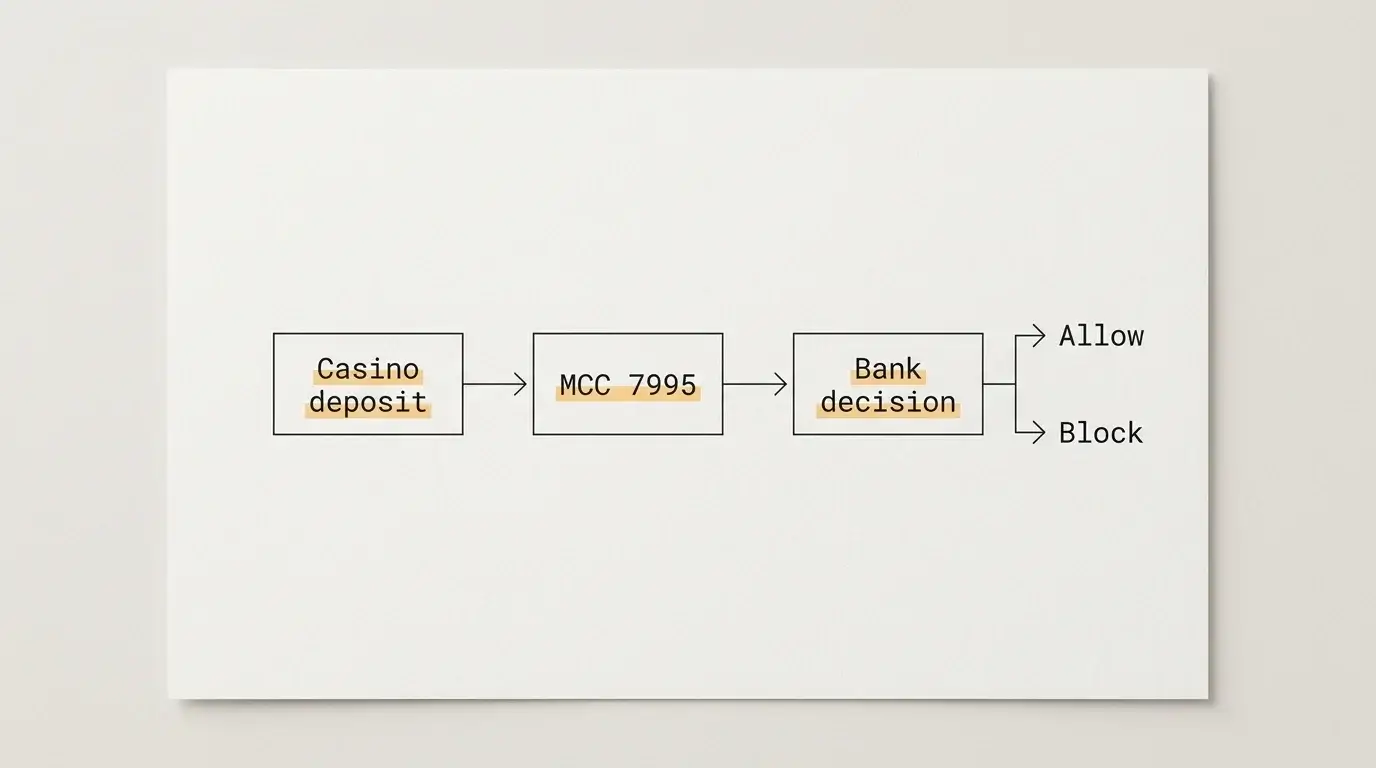

The first thing to understand about any payment card and any casino is the merchant category code — MCC 7995 — which is the four-digit identifier Visa and Mastercard apply to gambling transactions. Every card transaction carries an MCC, and issuing banks use it to apply category-level controls. UKGC-licensed casinos universally code their transactions as 7995. Non-GamStop casinos are supposed to, and most do, but the picture is less consistent than it should be — some operators route payments through processors that classify the transaction under a more generic code, and that is the technical loophole that lets some offshore deposits slip through controls that would block a UKGC transaction.

Revolut reads MCC 7995 transparently. When a transaction arrives carrying that code, Revolut applies whatever rules the account holder has configured — and the default for a new Revolut account is that gambling transactions are permitted unless the user has switched on the gambling-block toggle. Where things get interesting is the small fraction of offshore casinos using non-7995 routing. Those transactions look to Revolut like a generic card-not-present purchase from an international merchant, which is processed under standard rules with no gambling-specific intervention.

The gambling-block toggle and the cool-off period

Revolut’s gambling-block feature sits inside the security settings of the app, and it is one of the more thoughtful pieces of consumer-protection tooling in UK banking. Toggling it on does two things — it blocks all subsequent transactions that arrive with MCC 7995, and it imposes a cool-off period before the block can be removed. The cool-off in 2026 sits at 48 hours, which means a player turning the block on cannot turn it off the same evening to chase a session. The friction is the point.

The cool-off was originally added because Revolut’s data showed that instant on-off toggling defeated the purpose — players were turning the block off in the middle of a session and turning it back on the next morning. The 48-hour window is long enough that the impulse passes for most users. For UK players who took offshore as a route around UKGC affordability checks — the new £150 net-deposit threshold introduced in February 2025 has been the single biggest driver of that migration — the gambling block is the closest thing they have to a self-imposed circuit breaker that actually works.

The block is per-currency-account on Revolut, which is a detail worth knowing. If you have both a GBP account and a EUR account inside Revolut, the block needs to be applied to both — or, more reliably, applied at the Revolut user level rather than per currency. Newer versions of the app expose this as a master toggle rather than per-pocket, but older Revolut users sometimes still see the per-currency settings, and a per-pocket block does not stop a transaction that runs against a different pocket.

Revolut as a deposit method and its typical outcomes

The actual deposit experience on a non-GamStop casino paying with Revolut breaks down into roughly four scenarios. First, the casino runs MCC 7995 and you have the gambling block off — the transaction goes through normally and credits your casino balance in seconds. Second, the casino runs MCC 7995 and you have the block on — the transaction is rejected at Revolut’s end with a declined status. Third, the casino routes through non-7995 — the transaction goes through regardless of your gambling-block setting, which is the scenario that quietly defeats the protection. Fourth, the casino is in a region Revolut flags as high-risk — the transaction can be held for additional verification, sometimes for several hours.

The fourth scenario is the one growing in 2026. Revolut has tightened its risk scoring on transactions to offshore gambling jurisdictions over the past year, in part because of pressure from regulators and in part because Grainne Hurst, who runs the Betting and Gaming Council, has been pushing UK financial institutions hard on the question — her line, repeated across press appearances, is that “what we are seeing is a harmful black market scaling up at pace. Illegal operators are becoming more sophisticated, more visible and more aggressive in how they reach UK customers. That should concern anyone who cares about consumer protection.” Revolut is one of the institutions that has responded to that pressure with sharper transaction monitoring, and players reporting one-off declines on previously working casinos are usually seeing the effect of an updated risk model rather than a permanent ban.

Revolut as a withdrawal target

Withdrawing to a Revolut card from a non-GamStop casino is mechanically the same as withdrawing to any UK debit card, with a small wrinkle. Revolut accepts inbound card payments through Visa Direct and Mastercard Send rails, which most offshore casinos use for card payouts. The timing is usually under an hour on the Revolut side once the casino has broadcast the payment.

The wrinkle is that Revolut treats incoming gambling-related payments with the same MCC tagging logic as outgoing, and a large or unusual incoming payment from an offshore gambling jurisdiction can trigger an account review. The review is rarely fatal — Revolut is asking you to confirm the source of funds and provide documentation, which is a routine AML process — but it can delay access to the money for two or three working days. For a player who has just won and wants to withdraw, that delay is uncomfortable in a way that the deposit-side friction is not.

The other option some operators offer is paying out to a Revolut account via bank transfer rather than card. The receiving leg is a standard Faster Payments inbound, which Revolut handles the same way any other UK bank does. That route avoids the card-rail processing time but takes longer at the casino’s end because bank transfers are usually batched into a daily payout run.

Monzo, Starling and Wise as alternatives

Revolut is the most discussed of the UK challenger banks at offshore casinos, but it is not the only one. Monzo, Starling and Wise have their own positions on gambling, and the practical experience differs from Revolut’s in meaningful ways. Monzo offers a gambling block with a similar cool-off design and applies it strictly to MCC 7995 transactions. Starling has a gambling block toggle and tends to be slightly more aggressive in declining offshore-coded transactions, regardless of the block’s state. Wise is the most permissive of the four, primarily because it sees itself as a money-transfer service rather than a current account, and its merchant-category controls are lighter as a result.

![]()

For a player evaluating which account to use, the comparison comes down to what role you want the bank to play in your gambling. A challenger bank with strong category controls is a working safety layer if you want one. A bank with light controls makes the offshore route smoother but removes that layer entirely. Neither is the right answer in the abstract — they are different tools for different intentions. The role of the underlying card type sitting behind any of these accounts is a separate conversation entirely, and the picture for credit cards at offshore casinos is materially different from the debit-card and challenger-bank story.

Will Revolut close my account if it sees offshore casino transactions?

Closure for offshore gambling activity alone is rare — Revolut’s standard response is to ask for source-of-funds documentation if transactions reach a flagging threshold, not to close the account. Closures do happen, but usually in conjunction with other risk signals like high-value transactions to unrelated jurisdictions or inconsistencies in account information. A handful of medium-sized gambling transactions on a documented account is not, on its own, a closure trigger in 2026.

How long is Revolut’s gambling-block cool-off period in 2026?

The cool-off is 48 hours. Once you turn the gambling block on, you cannot turn it off again until 48 hours have elapsed from the activation timestamp. The design is deliberate — short enough that the friction is endurable for someone who genuinely changed their mind, long enough that an impulse to chase a session at midnight cannot be acted on the same night. The clock is per-user and not affected by app reinstallation or logout.

This material was created by the OFFSTAKE team.

Related posts

The Curaçao LOK Reform Explained: What 2024–2026 Changes Mean for UK Players

Bingo Sites Not on GamStop: Room Structures, Chat-Host Models and Offshore Bingo Economics